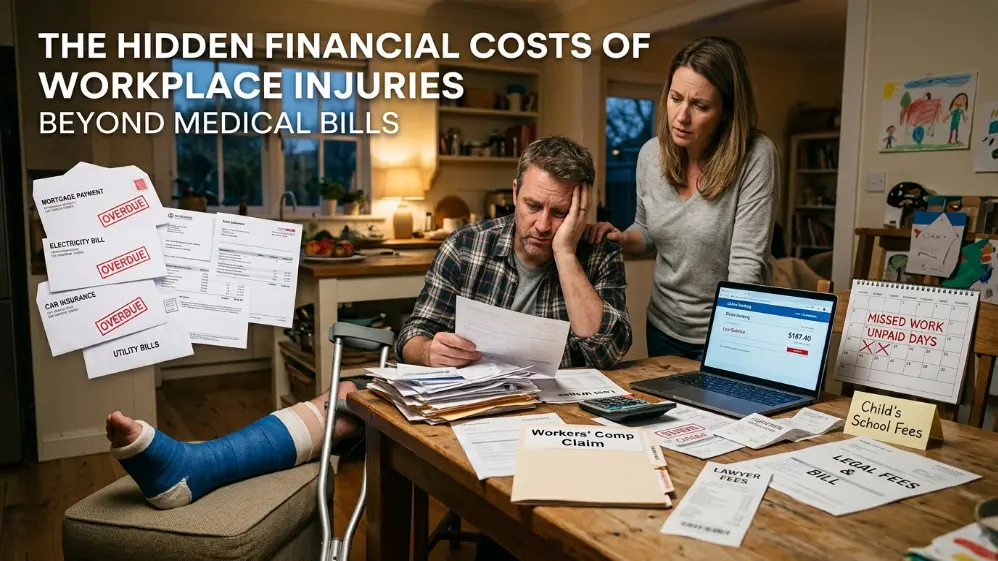

Most people think a workplace injury means one big medical bill. That is not the full picture. The hidden financial costs of workplace injuries run far deeper than any single invoice.

The National Safety Council (NSC) reports that work-related injuries cost the U.S. economy $181.4 billion in 2024. Of that total, wage and productivity losses made up $54.9 billion. Medical expenses accounted for only $36.8 billion. In other words, money lost from missed work outweighs the medical bills themselves.

A joint study by Liberty Mutual and Harvard University found that for every $1 in direct injury costs, workers and employers absorb $2.12 in indirect costs. OSHA estimates that the multiplier rises to 4 to 6 times the direct cost in many workplace injury cases.

If you were hurt on the job, knowing what you have truly lost is the first step to protecting yourself. The Law Office of Edward Seplavy helps injured workers find and recover every category of loss, not just the ones covered by a receipt.

Why Are Medical Bills Just the Tip of the Iceberg?

Medical bills feel overwhelming. But workers’ compensation usually covers them, at least in part. That can make injured workers think their financial exposure is limited. It is not.

Direct costs include emergency care, hospital stays, surgery, physical therapy, prescriptions, and specialist visits. These are the costs you can see and track.

The National Council on Compensation Insurance (NCCI) reports that the average workers’ compensation claim in 2022 to 2023 cost $47,316. Claims involving head and central nervous system injuries averaged $90,043 each. But these figures only reflect what insurance paid. Hidden costs sit on top of all of them.

The 8 Most Significant Hidden Financial Costs of Workplace Injuries

1. Lost Wages and Reduced Income

Workers’ compensation does not replace your full paycheck. According to wage replacement data from the Social Security Administration, most states replace only 60% to 75% of pre-injury wages.

A worker earning $55,000 who misses six months loses about $27,500 in gross income. Workers’ compensation replaces $16,500 to $20,625, leaving a shortfall of $6,875 to $11,000. This gap is seldom addressed in claims.

The problem is even worse for hourly workers, shift workers, and people who earn overtime, commissions, or tips. Workers’ compensation often leaves those income sources out of the calculation entirely.

2. Long-Term Career Disruption and Reduced Earning Capacity

Some injuries permanently limit a worker’s job abilities. For example, a construction worker with a herniated disc may not lift heavy materials again. A delivery driver with a knee injury may lose higher-paying routes. A nurse with a rotator cuff tear may face permanent restriction.

Reduced earning capacity is the gap between pre- and post-injury income. Over 20 years, a $10,000 yearly reduction totals $200,000 in economic loss. Standard claims rarely capture this amount.

3. Retraining and Career Transition Costs

When returning to the same job is physically impossible, injured workers face two options. They can retrain for a new career, or they can accept lower-paying work they can still perform.

Both options cost money. For instance, paralegal and HVAC certification programs each have fees. Add vocational rehab, licensing, and lost income during transition. These expenses are rarely included in workers’ compensation claims.

4. Out-of-Pocket and Daily Hidden Expenses

Not every cost comes as a formal medical bill. Some costs pile up slowly in small amounts. The 6 most common out-of-pocket costs injured workers overlook are:

- Transportation: gas, parking, and rideshare for medical visits, averaging $15-$50 per visit across 20-50 visits.

- Over-the-counter medications: pain relievers, anti-inflammatory creams, and sleep aids are not covered by insurance.

- Home modification expenses: grab bars, shower chairs, stair railings, and ramp installations needed during recovery

- Domestic support costs: housekeeping, childcare, lawn care, and meal delivery when the injured worker cannot do those tasks

- Recovery supplements: dietary products and prescribed nutritional changes

- Increased food costs: prepared meals and convenience foods when cooking becomes too painful or difficult

A worker going to physical therapy three times a week for three months can spend $1,350 to $4,500 on transportation alone. That is before a single co-pay is counted.

5. Psychological and Emotional Trauma Costs

Workplace injuries affect more than the body. They affect the mind too. Workers’ compensation systems rarely cover these costs.

Post-traumatic stress disorder (PTSD), anxiety, depression, and adjustment disorders are all documented outcomes after serious workplace injuries. This is especially common after machinery accidents, falls from height, chemical exposure, or workplace violence.

Psychiatric care costs $150 to $300 per session out-of-pocket. Six months of bi-weekly therapy adds up to $1,800 to $3,600 in mental health costs. Research also shows that workers who develop depression after an injury recover physically at a significantly slower rate. Slower recovery means longer wage replacement periods and higher total costs overall.

6. Family and Household Financial Disruption

A workplace injury not only hurts the injured worker. It affects the whole family.

A spouse or partner who cuts back work hours to help with caregiving loses income, too. That secondary income loss can reach $10,000 to $25,000 per year. No workers’ compensation claim addresses that.

Families also take on credit card debt, drain savings accounts, and postpone retirement contributions. Children miss out on after-school programs, tutoring, and activities. Each of these costs exists because of the workplace injury.

7. Chronic Health Costs and Long-Term Medical Management

Many workplace injuries do not heal and disappear. They turn into long-term conditions with ongoing costs.

A herniated disc may need epidural steroid injections every six months. Each procedure costs $1,500 to $3,000. A traumatic brain injury may require neurological management, cognitive rehabilitation, and occupational therapy at $5,000 to $15,000 per year. A serious burn injury may need multiple reconstructive surgeries over five to ten years.

Chronic pain conditions develop in a large share of workers with serious musculoskeletal injuries. Workers’ compensation claims often close before these long-term needs show up. When that happens, injured workers are left to pay those future costs on their own. An experienced workers’ compensation attorney documents projected future medical needs before any settlement is signed.

8. The Legal and Administrative Cost of Navigating Claims Alone

Workers without legal representation almost always recover less than those who hire an attorney. Insurance carriers have claims adjusters and legal teams. Their job is to reduce what the company pays out.

The 4 most costly mistakes injured workers make without legal guidance are:

- Accepting the first settlement offer without knowing what future medical costs will look like

- Failing to document all injury-related expenses, including out-of-pocket and indirect costs

- Missing filing deadlines can permanently remove certain legal rights.

- Returning to work too early under insurance pressure, which can cut or end benefits

Most workers’ compensation attorneys work on a contingency fee basis. There are no upfront costs. Legal fees come from the settlement, not from the injured worker’s own pocket.

What Workers’ Compensation Does Not Cover and What Legal Action Can Recover?

Workers’ compensation covers medical costs and partial wage replacement. That is it. A personal injury or third-party liability claim can recover much more, including:

- Full lost wages at 100%, not the 60% to 75% workers’ comp rate

- Pain and suffering damages, which workers’ compensation does not pay at all

- Loss of enjoyment of life, a recognized legal category of recoverable damages

- Future earning capacity, calculated over the rest of your working years

- Punitive damages when an employer acted with gross negligence or willful disregard for safety

- Loss of consortium claims for family members when the injury affects marital or parental relationships

Sometimes a third party caused or contributed to the injury. That could be a contractor, equipment manufacturer, property owner, or delivery company. In those cases, a separate personal injury claim can run alongside the workers’ compensation claim. That second claim often results in a much larger financial recovery.

7 Steps to Protect Your Financial Recovery After a Workplace Injury

Take these 7 steps right after a workplace injury to protect your full financial recovery:

- Report the injury in writing to your employer the same day it happens.

- Document all expenses in a notebook or app, including every co-pay, mile, and out-of-pocket purchase.

- Photograph your injuries and the accident location before anything changes.

- Preserve all medical records, imaging reports, and treatment notes.

- Track every missed shift with dates, hours, and dollar amounts.

- Do not give recorded statements to insurance adjusters before speaking to an attorney.

- Consult a workplace injury attorney before signing any settlement or return-to-work agreement.

How the Law Office of Edward Seplavy Helps Injured Workers Recover Every Dollar?

At the Law Office of Edward Seplavy, our workers compensation lawyer Lexington SC looks at a workplace injury the way it really is. It is not one bill. It is months or years of financial loss piling up across wages, career potential, daily expenses, and family stability.

We start with a full financial audit of every loss category. We go beyond the workers’ compensation claim. We look at third-party liability claims, employer negligence claims, and product liability actions, too.

There are no upfront legal fees. You pay nothing unless we recover compensation for you.

Injured on the job? Contact the Law Office of Edward Seplavy today for a free consultation. The hidden financial costs of workplace injuries are real, documented, and legally recoverable.

Also Read

Add a Comment